Here are five bad habits in insurance according to HK’s insurance regulator

These habits drag down Hong Kongers insurance literacy rate.

For a market ranking first globally in insurance penetration according to research firm Swiss Re Institute, it is surprising that Hong Kong’s insurance literacy rate stood only at 52%.

In the 2022 Report on Insurance Literacy Tracking Survey (ILTS) in Hong Kong 2021 by the Insurance Authority (IA), it was found that most, Hong Kongers are moderately literate when it comes to insurance.

“There was a general understanding about policyholders’ rights, insurance principles and product features, but limited knowledge of risk exposure and protection needs,” the IA said.

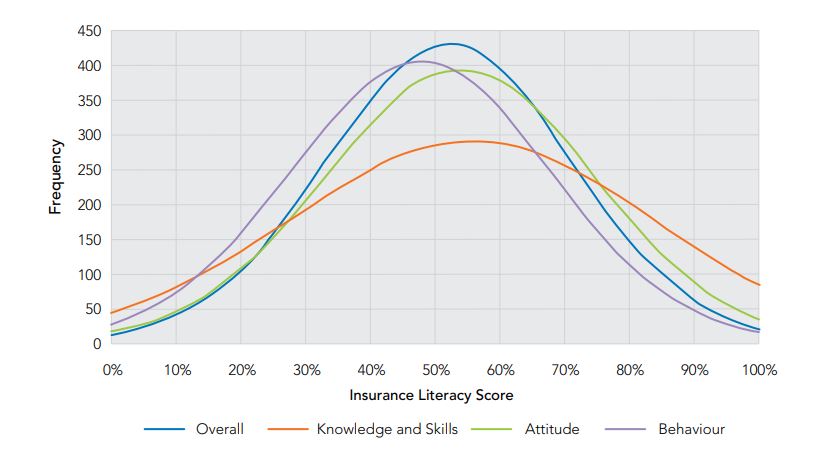

Findings and bad behaviours

Respondents of the ILTS were analysed based on the three dimensions of insurance literacy—knowledge and skills, attitude, and behaviour. The results revealed that bad insurance behaviours exhibited by Hong Kongers is the culprit dragging down the insurance literacy rate of the city.

For example, the survey revealed that when it comes to buying insurance, 72% of respondents relied on the advice and experience drawn from family members or friends instead of insurance or financial professionals. IA identified this as the first behavioural bias—over-reliance on informal information sources.

Consumers who are overly reliant on their family or friends for information and advice is a sign of bandwagon effect. mMeaning, that these people do something primarily because others are doing so, regardless of their own beliefs, IA said.

“People often want to be on the winning side when they make a decision. As a result, they look towards their family or friends to see what is right and then jump on the bandwagon,” the IA explained.

The second behavioural bias is Hong Kongers’ too much focus on promotions. Promotions offered by insurance companies affect consumers’ decisions via price complexity and misdirected attention. The former means consumers find it challenging to calculate true prices when they face multiple prices, such as discounts and add-ons, leading to confusion and increased possibility of errors. The latter means promotions reduce consumers’ motivation for mental effort, resulting in choices becoming less deliberate but driven by emotions and feelings.

Most consumers also seldom shop around for better insurance deals when purchasing or renewing insurance. Only 43% of respondents tended to compare different insurance products, whilst nearly half of the policy-holding respondents were influenced by promotion campaigns such as premium discounts, complimentary movie tickets, and healthcare services offered by insurers. On the other hand, a mere 15% of general insurance policy-holding respondents reviewed renewal terms carefully and shopped around when they renewed their policies.

Consumers also tend to procrastinate. This can be caused by different reasons such as too many choices leading to being overwhelmed or people postponing making a decision about insurance as they find it emotionally stressful.

Next is passiveness and inertia. The complexity of terms and conditions makes policy comparison very time-consuming. Moreover, policyholders often renew their policies with their current insurers due to a perception that switching is risky and with preference for the familiar rather than the best deal.

The last is that most consumers do not take the time to read the terms and conditions of their policies as many find this too long and time-consuming in addition to being written in complex legal languages. The perception most consumers think is that no one reads T&Cs or that they have no choice but to accept them thus there is no point in reading them.

Only 32% of policy-holding respondents read and study T&Cs before committing to acquire insurance coverage. 20% read neither policy details nor brochures. The rest simply focused on brochure information and verbal advice from agents, brokers, family members, or friends.

Demographical factors

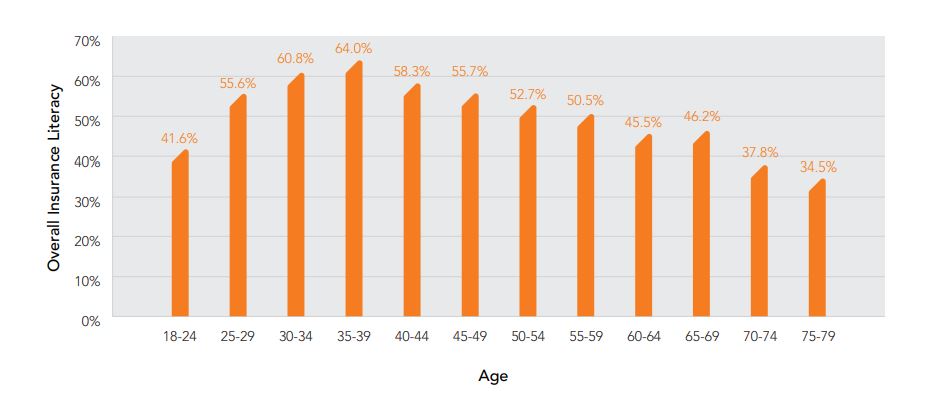

IA also found that insurance literacy can be affected by demographic factors such as age, education, and income.

The youngest and the oldest have the lowest literacy scores. Those ages 18 to 24 have a literacy score of around 42% whilst those ages 60 to 79 score below 50%. In contrast, are those people in their 30s who have insurance literacy scores of above 60%.

Income is also positively correlated to insurance literacy as the higher one's income is, the higher the literacy rate. The literacy score of respondents with a monthly income level below HK$10k is 41%, whilst those earning HK$100k or above score 80%.

The report also found that insurance literacy is correlated to educational level. For respondents who graduated only from primary schools, their insurance literacy score was below 35% whilst those who graduated from tertiary education or above scored 63%.

Similar results

Talking to Hong Kong Business, Danny Lee, Chief Product Officer at Manulife Hong Kong and Macau said the key findings of the IA’s study mirror a study they did in February which revealed that most Hong Kong taxpayers do not still do not fully understand the characteristics and benefits of tax-deductible products.

Danny Lee, Chief Product Officer at Manulife Hong Kong and Macau.

Manulife’s survey asked Hong Kong taxpayers about their knowledge of a trio of tax-deductible solutions: Voluntary Health Insurance Scheme (VHIS), Qualifying Deferred Annuity Policies (QDAP), and Tax Deductible Voluntary Contributions (TVC) under Mandatory Provident Fund (MPF) schemes.

“Respondents on average answered just four out of fifteen questions correctly. With an increasing variety of products in the market, we would advise people to take the time and effort needed to educate themselves on these solutions so they can better understand their options and plan ahead,” Danny said.

Danny also stressed that it is important to seek professional advice from financial advisors who have the knowledge and experience to help customers create a suitable insurance portfolio based on their needs.

This survey by Manulife is also how they, as a major insurer in Hong Kong are striving to educate the public about the risks of being unprepared for future health and financial challenges.

“Hong Kong is one of the most sophisticated insurance markets in the world. IA’s finding means that some Hongkongers are failing to make good use of the diversified products available in the market to achieve sufficient risk protection planning. Protection planning is an important part of one’s financial planning, particularly in a place like Hong Kong where the cost of living and medical expenses are relatively high. Life and medical insurance can help to close the protection gap. It is crucial to act early and make good use of a wide range of insurance solutions to hedge the risk exposure,” Danny said.

“The pandemic has increased the number of people in Hong Kong adopting healthier lifestyle habits and boosted awareness of health and financial protection, which we believe will raise the level of literacy and overall positive attitude over the next decade,” he added.

Advertise

Advertise