Why Hong Kong’s retail recovery is taking longer than expected

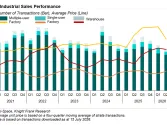

Total retail sales decreased by 7.1% YoY.

The retail sector in Hong Kong is facing a slower-than-expected recovery, with persistent economic challenges weighing heavily on consumer spending, according to Knight Frank.

Total retail sales for the first eleven months of 2024 amounted to $344b, marking a 7.1% decline compared to the same period in 2023.

Durable consumer goods bore the brunt, posting an 11.8% drop, whilst discretionary categories such as department stores and jewellery also suffered double-digit declines. The luxury retail segment, in particular, has struggled amidst the tough economic landscape.

Meanwhile, sales of medicines and cosmetics, classified under "other consumer goods," showed resilience with a 5.1% increase during the same period, highlighting varying consumer spending patterns amid ongoing market challenges.

Visitor arrivals in 2024 reached approximately 45 million, fuelled in part by the reinstatement of the multiple-entry scheme for Shenzhen residents and the scheduling of world-class mega-events.

Despite this, local outbound travel surged by 23%, driven by a strong Hong Kong dollar and the recovery of airline capacity.

As traditional retailers grapple with sluggish sales, online enterprises are making strategic moves into physical spaces to boost their visibility. Singapore-based online securities trading platform Longbridge recently opened its flagship store, Longbridge Space, at Unit 3, 26 Nathan Road, Tsim Sha Tsui. The 8,500 sq ft space spans two floors and commands a monthly rent of $1m.

Moreover, luxury retailers remain cautious about expansion, creating opportunities for service providers like financial and insurance firms to establish street-level visibility.

Market headwinds are expected to persist into 2025, with no immediate stimulus to reinvigorate the sector. Landlords of shopping centers are urged to focus on unique selling propositions to retain local clientele and attract tourists, maintaining high occupancy rates.

Meanwhile, tenants—especially service providers—are advised to capitalise on vacancies in prime locations to enhance their visibility.

“In 2025, leasing transactions are expected to gradually increase,” the report said. “However, rents are unlikely to rise, as the majority of the retail sector remains in recovery mode.”

Advertise

Advertise